FTX Bankruptcy Court Filings Reveal Over $3 Billion in Creditor Debts

The crypto exchange FTX has disclosed that the firm is in debt to its top 50 creditors for $3.1 billion total, according to bankruptcy court filings.

In spite of the fact that the court document did not reveal the names of those affected by the sudden collapse of FTX, the document identifies the extent of the financial losses for the exchange’s clients.

It is estimated that FTX’s ten largest creditors have unsecured claims of more than $100 million each, with a total debt of over $1.45 billion, the document states. The filing clarified that the debt is not owed to company insiders, and the information may change as more details become available.

FTX has a debt of $276 million to its largest creditor and $21 million to its 50th largest one. Yet, there is a possibility that the document is only the tip of the iceberg in terms of what the company owes in reality since the exchange admitted the previous week that it might have over a million creditors.

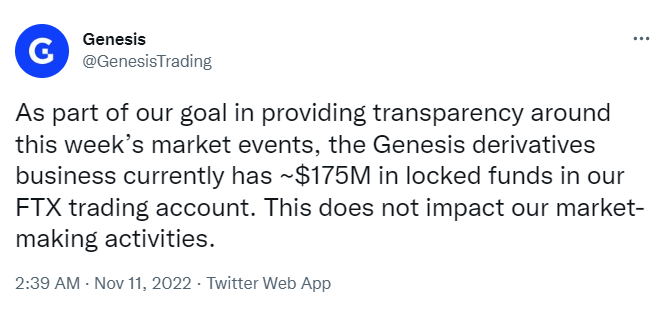

According to the document, FTX owes $174 million to the third-biggest creditor, whose identity is not disclosed. Although the figure has not been confirmed, it is in line with a statement that cryptocurrency lender Genesis made two weeks ago: Genesis held $175 million worth of FTX.

The company explained in its bankruptcy document that the management team under the new CEO, John J. Ray III, calculated the totals based on information that was viewable but not accessible. Currently, the company does not have complete access to the data of its customers.

Furthermore, the management team said that debt figures could be inaccurate since some creditors may have already received their payments, but it isn’t reflected in the company’s accounts.

A related motion was filed earlier to redact the names and personal information of the creditors of FTX.

There is a concern that sharing creditor information could alert unscrupulous businesses to the situation.

“Public dissemination of the Debtors’ customer list could give the Debtors’ competitors an unfair advantage to contact and poach those customers, and would interfere with the Debtors’ ability to sell their assets and maximize value for their estates at the appropriate time,” the statement said.

FTX was also pointed out in the motion for not keeping track of customer data accurately enough to figure out who owed what.

“The Debtors historically did not keep appropriate books and records, and the Debtors are currently working to access certain sources of data and records that are currently unavailable.”

As stated in the motion, FTX decided to compile its creditors into one file because of overlapping creditors across its Chapter 11 cases, an unorganized record management system, and a lack of time and resources.

“Creditor information, and in particular customer information, is not clearly labeled or identifiable by [FTX],” the document states. “As a result, presenting the information on a consolidated basis will ensure the most relevant and known information can be promptly disclosed.”

An FTX bankruptcy hearing date was set in court documents filed on Sunday. A court hearing will take place on Tuesday in Wilmington, Delaware.