The Wash Sale Rule Explained: Does It Cover Crypto Too?

Growing wealth, owning shares in successful businesses, and building an array of investments can be exciting until it’s time to pay capital gains taxes. Handling multiple income sources might seem appealing, but the burden of taxes often brings us back to earth.

However, the U.S. tax code does have a bright spot: if your investment is losing money, you can sell it to lower your taxable income. But be careful! If you sell an asset at a loss and then buy the same or a very similar investment quickly afterward, you could run afoul of the wash sale rule. This rule is often overlooked by new investors, leading to unwelcome consequences.

So, it’s essential to understand the wash sale rule in detail and, importantly, explore if it applies to the rapidly changing world of cryptocurrency.

Key Takeaways

- The IRS wash sale rule prevents artificial tax loss creation by disallowing loss claims on repurchased identical securities within a specific timeframe.

- The wash sale rule is triggered when an investor sells a security at a loss and repurchases a substantially identical security within a 30-day window.

- To avoid triggering the wash sale rule, investors can wait for a full 30-day period before repurchasing the same or similar security, opt for materially different investments, or consider strategic selling and buying dates.

- Currently, crypto investments evade the wash sale rule, but regulatory changes are expected to include them in the near future.

Wash Sale Rule From A to Z

The wash sale rule is a regulation put in place by the Internal Revenue Service (IRS) in the United States. Its purpose is to stop investors from taking unfair advantage of tax breaks when dealing with investments that have lost value.

Under this rule, if investors sell an investment at a loss and then buy the same or a substantially similar investment within 30 days, they are not allowed to deduct that loss from their taxes. Instead, the loss must be included in the cost basis of the new investment. This then impacts the calculation of gain or loss when they decide to sell the new investment in the future.

In essence, the wash sale rule prevents investors from manipulating the system for short-term tax benefits by selling a security at a loss and quickly buying a virtually identical one.

What Is Cost Basis?

Cost basis is a term that relates to the original value of an asset, like a stock or cryptocurrency, which becomes crucial when calculating taxable gains or losses when the asset is sold or otherwise disposed of.

This original value is usually the price the asset was purchased, and it includes any costs associated with buying it, such as fees or commissions. If the asset was received as a gift or inheritance, the cost basis may be adjusted to match the asset’s fair market value when it was acquired.

The cost basis plays a critical role when an asset is sold. The difference between the sale price and the cost basis determines whether the investor has made a capital gain or a loss. If the sale price exceeds the cost basis, the investor has made a capital gain and may owe taxes.

Conversely, if the sale price is lower than the cost basis, the investor has made a capital loss, which can be used to offset capital gains and reduce the overall tax obligation.

What Is “Substantially Identical” Security?

The phrase “substantially identical” in the context of the wash sale rule is often confusing for investors. In its Publication 550, the IRS deals with capital gains and losses but doesn’t define what it considers “substantially identical.” Instead, it generally states that stocks or securities of one corporation are not typically regarded as identical to those of another corporation. However, there can be exceptions.

For instance, a company’s preferred stock could be substantially identical to its common stock if it shares certain characteristics. If the preferred and common stocks have equivalent voting rights or if the preferred stock can be converted into common stock, then the IRS may see them as essentially the same. This can happen if you sell one to buy the other to realize losses.

It’s also worth noting that attempting to circumvent the wash sale rule by selling investments in your taxable brokerage account and repurchasing them in an individual retirement account (IRA) owned by you or your spouse won’t work. If you’re within the 30-day window and the IRS sees the new investment as the same or substantially identical, it will still be a wash sale transaction.

How The Wash Sale Rule Works?

The wash sale rule is designed to inhibit taxpayers from creating contrived losses from selling securities while essentially keeping their position intact in those securities.

The rule operates within a 61-day window, including 30 days before the sale transaction and 30 days after. Once this period elapses, transactions involving the same or similar security are no longer subject to the wash sale rule.

While a loss might be disallowed due to the wash sale rule, it’s important to note that the disallowed loss gets added to the cost of the new purchase that activated the rule. When that new position is sold, any resulting loss can be deducted from taxes. Thus, the initial loss can be viewed as deferred rather than entirely forfeited.

Notably, the wash sale rule applies to selling options too, treated similarly to stocks, where a loss is realized, and identical options are reacquired within the 30-day period.

Essentially, if you had planned on using a loss to offset your capital gains or decrease your taxable income, the wash sale rule could upset this strategy, potentially leading to a higher tax obligation. However, there can still be a silver lining to a wash sale.

The amount of your loss can be added to the cost of repurchasing the same or a substantially identical investment, thereby increasing your cost basis. This might result in paying fewer capital gains tax later or claiming a larger loss if you sell the investment at a loss in the future.

For instance, let’s say you own 150 shares of ABC Inc with a cost basis of $15,000, and you decide to sell them on September 1 for $4,000, resulting in an $11,000 loss. If these shares are in a taxable brokerage account, you could normally claim this loss on your tax return.

However, if you choose to repurchase shares between September 2 and October 1, the wash sale rule comes into effect, disqualifying your loss from being tax-deductible.

The same principle applies if you buy shares within 30 days before the sale; if you purchased an equal amount of shares to those sold on September 1, anytime on or after August 2, the wash sale rule would apply, nullifying your ability to claim the loss on your taxes.

How To Prevent The Wash Sale Rule Violations

If you wish to sidestep the complexities of the wash sale rule, there are several strategies you can adopt. These approaches can help ensure that your investment decisions do not unintentionally activate the rule, leading to potentially unforeseen tax implications.

- Hold Off for 30 Days

The most straightforward way to prevent a wash sale is by simply waiting 30 days after selling an investment before repurchasing the similar or the same asset.

This strategy also requires you to refrain from buying the same or a similar investment on the day you sold, as well as during the 30 days preceding your sale. If you’re itching to reinvest immediately, consider putting your money into a markedly different asset.

- Seek Out Significantly Different Investments

The IRS isn’t explicit about what constitutes “substantially identical,” but the intention is clear: it doesn’t want you to claim a tax break for a sale that isn’t a genuine loss.

Therefore, if you’ve sold an investment, like one in the tech sector, look for another tech investment that differs significantly from the one you sold to dodge a wash sale. This could also be achieved by investing in a fund representing the same or a similar sector to the stock you sold.

For added safety, consider investing in an entirely different industry or sector. Consulting with a financial advisor or tax professional could be beneficial if you’re uncertain about how distinct your alternative investment needs to be. Automated investment services, or robo-advisors, can also handle tax-loss harvesting on your behalf.

- Develop A Long-term Investment Plan

Investors without a contingency plan for short-term market downturns might inadvertently trigger the wash sale rule by selling off in a panic and then rebuying the same investment once the market begins to recover.

Establishing a long-term investment strategy and sticking to it, even during market slumps, can assist you in making optimal investment and tax decisions, irrespective of market conditions. This approach promotes disciplined investing and reduces the likelihood of decisions driven by short-term market fluctuations, thereby reducing the risk of triggering the wash sale rule.

- Employ Dollar-Cost Averaging

Dollar-cost averaging (DCA) involves investing a set amount of money at regular intervals, irrespective of the security price. This strategy can help avoid the wash sale rule as it mitigates the likelihood of large, impulsive buys within the 30-day window.

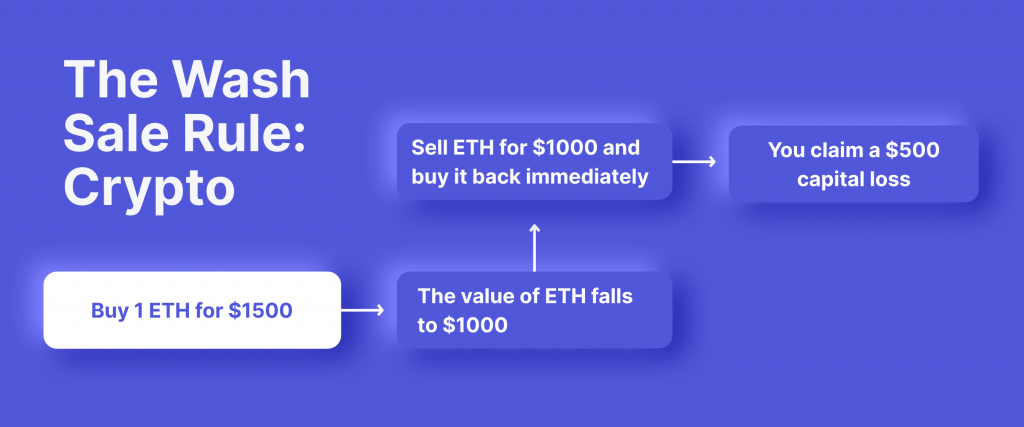

Does The Wash Sale Rule Apply To Crypto?

As it stands today, the wash sale rules do not apply to cryptocurrencies. However, it’s important to note that legislators have flagged this exclusion, as it potentially facilitates a tax evasion avenue for crypto investors, leading to substantial tax revenue shortfalls.

Steps are being taken to close this gap; notably, the 2024 Budget proposed by the Biden administration incorporates a provision to extend the wash sale rule to include cryptocurrencies.

While the precise timeline for when the crypto wash sale rule might be released remains uncertain, there’s no doubt that this crypto tax loophole has caught the attention of regulators and is likely to be sealed sooner rather than later. Therefore, staying informed and avoiding unnecessary tax charges is crucial.

How To Minimize Crypto Taxes

Even though the wash sale rule doesn’t currently apply to cryptocurrencies, this doesn’t mean these digital assets are exempt from taxation. The IRS treats cryptocurrency as property, usually taxed as an asset. This means you need to pay taxes on the profits you make when you sell or get rid of cryptocurrency.

For instance, let’s say you bought Bitcoin for $20,000 and later sold it for $30,000. You would have to pay tax on the $10,000 profit you made.

It’s important to note that these taxes are split into short-term and long-term categories. If you hold onto a cryptocurrency for less than a year, it’s considered short-term. But if you keep it for more than a year, it’s considered long-term. The tax rates are usually better for long-term holdings.

Dealing with cryptocurrency taxes can be complicated, so let’s get through some tips to help you manage your cryptocurrency taxes.

- Leverage Tax-Advantaged Accounts

One effective method for managing crypto taxes is to take advantage of tax-efficient instruments like Individual Retirement Accounts (IRAs). IRAs are essentially savings accounts with certain tax benefits not present in regular savings accounts.

For instance, a Traditional IRA allows holders to defer tax payments on capital gains until the funds are withdrawn during retirement, thanks to tax-deductible contributions.

On the other hand, a Roth IRA allows for tax-free withdrawals, given contributions are made after tax. This also implies that any profits made within a Roth IRA, such as profits from Bitcoin appreciating, remain untaxed, subject to specific conditions.

- Adopt a Long-Term Investment Mindset

A long-term investment strategy can either eliminate or significantly reduce your tax liabilities. You can avoid tax by not selling your crypto holdings since it’s only calculated on realized capital gains. However, this approach could be limiting as it restricts access to your crypto for spending purposes.

A more appealing alternative for many is to hold onto their crypto for long enough (typically one year or more) to qualify for a lower long-term capital gains tax rate.

Single individuals with a taxable income of less than $44,625 aren’t required to pay any capital gains tax, while those earning between $44,625 and $459,750 only need to pay 15% of their capital gains.

- Gift Crypto To Loved Ones

Another strategy for managing crypto taxes is gifting your cryptocurrency holdings. Giving a gift, whether Bitcoin or any other cryptocurrency, is typically not considered a taxable event, meaning neither the gifter nor the receiver will have to pay taxes on the gifted amount.

However, there are limits to be mindful of. For instance, the current U.S. regulations allow you to gift up to $17,000 per person per year without filing a gift tax return. The recipient will still be required to pay tax on any gains after receiving the gift.

- Consider Relocating

Relocating to a different country is a more drastic measure to reduce or avoid crypto taxes, but it can be highly effective. Countries like Puerto Rico, a U.S. territory with a unique tax system, don’t levy taxes on capital gains from investing.

Hence, substantial profits from Bitcoin or other cryptocurrencies remain tax-free. On the other hand, Portugal, which also doesn’t tax profits from cryptocurrency investments, requires investors to establish residency to benefit from these tax laws.

- Use Crypto Tax Software

Lastly, consider using cryptocurrency tax software. These tools can automatically track crypto transactions, calculate capital gains or losses, and even generate tax reports.

This can significantly simplify preparing your taxes and help ensure you don’t overlook any potential deductions or credits. It’s important to keep records of all your transactions to ensure the information the software generates is accurate.

Wrapping Up

Today’s economic environment sees a multitude of cryptocurrency investors capitalizing on wash sales as part of their tax-loss harvesting game plan. This approach is a two-pronged tool: reducing tax obligations while maintaining a firm foothold in their crypto assets.

However, the tax rules concerning cryptocurrency are anything but static. With each passing day, the global regulatory environment is adapting to the rising prominence of cryptocurrencies, and changes in tax laws are an integral part of this evolution. Similarly, the wash sale rule, an aspect often given less attention in the crypto sphere, is now under the microscope.

Adapting to these changes can be challenging, but it’s essential to managing a crypto portfolio. As tax rules evolve, so should your strategies. The key is to stay vigilant, flexible and informed. Remember, in the rapidly evolving world of crypto, knowledge is not just power; it’s profit.